Rulefinder

Cross-Border Lending

Red flag analysis to help you optimise the structure of your lending and security activities

How it works

Rulefinder Cross-Border Lending is a comprehensive analysis of the legal and regulatory issues which impact how to structure cross-border lending and security activities.

Red flag issues are identified in an easy-to-use summary and underpinned by detailed analysis from leading local counsel around the world.

Topics covered include:

- How to take and hold security and collateral from an overseas borrower

- Key issues relating to enforcement, including the availability of self-help remedies, and restructuring regimes and toolkits

- Tax implications, with particular focus on withholding tax and stamp duty

- How to structure cross-border lending activities without triggering licensing, registration, or authorisation requirements, including:

- Loan origination, loan transfer, loan sub-participation and lender-to-lender activities

- The impact on the analysis of lender type, borrower type and location, loan nature and purpose and lending strategy

Who it's for

In-house legal teams and lending deal teams seeking to identify critical issues in cross-border lending, whether within a private credit firm/fund or a traditional bank.

How it helps

The information is updated daily by our dedicated team of experts, so you always have the latest position at your fingertips without having to incur the time and hassle of local lawyers.

Available as a simple annual subscription.

The CRD 6 tracker has been very useful, particularly when providing updates on countries of specific interest to our business colleagues.

Legal Counsel, Global Financial Services Firm

Product features

-

CRD 6 Tracker for Third-Country Firms

Be ready for the new branch requirement with our CRD 6 Tracker for Third-Country Firms.

The Tracker shows how EEA Member States are implementing the requirement - with clear, jurisdiction-by-jurisdiction insights.

Click 'Play' to learn more.

-

Simplify compliance

- User friendly, colour-coded on-screen report of key issues

- Impact-flagged daily updates, curated by our expert team

- Access to sources, including local counsel memoranda and contact details

- Compare and version audit features

-

AIFMD 2 Tracker

Are you tracking how EEA Member States are implementing AIFMD 2 – and what their expected positions are on key changes?

Our AIFMD 2 Tracker helps you stay informed with clear, up-to-date insights across jurisdictions, all in one place.

Click 'Play' to learn more.

Jurisdictions covered

We currently cover the below with Belgium and Canada coming soon.

Mexico, Bermuda and the Cayman Islands

Austria, Denmark, Finland, France, Germany, Ireland, Italy, Luxembourg, Netherlands, Norway, Portugal, Spain, Sweden and United Kingdom

ADGM, DIFC, Saudi Arabia, South Africa and UAE

Australia, India, Japan, Singapore and Vietnam

Product team

Experienced senior lawyers

Rulefinder Cross-Border Lending is led by a team of senior financial services lawyers, many of whom have been with aosphere for nearly a decade. They began their careers at top-tier law firms before branching into roles such as in-house counsel at financial institutions, knowledge/professional support lawyers, or as senior practitioners at a regulator. Many have trained and practised internationally.

Now specialists in comparative legal analysis, they assess whether and how firms can conduct cross-border financial services and identify trends in this complex, ever-evolving landscape.

This diverse expertise, combined with a strong collaborative ethos, ensures the quality, consistency and practical value of our content.

Penny Blair

Co-Head, FinReg Products

Jenny Ljunghammar

Co-Head, FinReg Products

Sharon Gowdy

Counsel - FinReg Products

Emily Hillson

Specialist FinReg Lawyer

Speed Read - Japan

Speed Reads, a popular feature of our Rulefinder products, give a handy, simple snapshot of the legal landscape in jurisdictions.

Enjoy this taster of a Rulefinder Cross-Border Lending Speed Read!

Topics covered

How are “lending activities” typically structured into a particular jurisdiction so that requirement for a lending/credit licence/registration/authorisation is not triggered?

Within scope are:

- loan origination

- loan transfers

- risk/sub-participations

- issuing bonds/notes

- lending to group companies of the borrower based in another jurisdiction

- use of securitisation structures/vehicles

- responding to reverse enquiries

- any other workarounds relevant to that jurisdiction

- granting of guarantees/letters of credit

- trade finance activities

Is it possible to conduct related activities (also without triggering requirement for licence/registration/authorisation)?

- marketing activities relating to the firm’s lending activities (e.g. via phone, fly-in, email) and whether particular disclaimers are required

- general marketing activities related to the firm’s brand and awareness-raising of product/service lines)

- definition of arranging/underwriting and any exemptions/exclusions

Does the analysis depend on the:

- type of lender (credit institution/fund/wholly-owned subsidiary – for funds relevant to also consider its domicile, whether open/closed-ended, regulated (e.g. ELTIF))

- type and location of borrower

- nature of loan (drawn/undrawn, secured/unsecured, performing/non-performing)

- purpose of loan (e.g. real estate finance, cash flow finance, rescue finance, litigation funding, to finance financial instruments)

- lending strategy (e.g. private debt, life sciences, ESG)

Practical issues that arise in terms of syndication/arranging e.g. whether requirements triggered by:

- responding to invitation from arranging bank to participate in a syndicate?

- lender-to-lender discussions and/or participation in loan syndication roadshows?

- organising or participating in activities with arranging bank, facility agent and/or security agent/trustee?

- acting as a facility agent?

Where licensing/registration/authorisation requirements are triggered, are there any mutual recognition, equivalence or passporting routes available?

What type of sanction/penalty could be incurred if activity is undertaken without a licence/registration/authorisation? Could transaction be void/voidable (if so, at whose instigation)?

Consideration of various issues relating to taking security/collateral:

- possible to take security from a borrower in the jurisdiction and if so whether it’s generally held directly or through a third-party?

- does analysis depend on whether charges are fixed or floating?

- is the role of security trustee/agent is recognised in the jurisdiction?

- is acting as security trustee/agent is a licensable activity?

- whether a change of lender or security agent/trustee will affect the security?

- are there types of assets over which security cannot be granted?

- must security be registered?

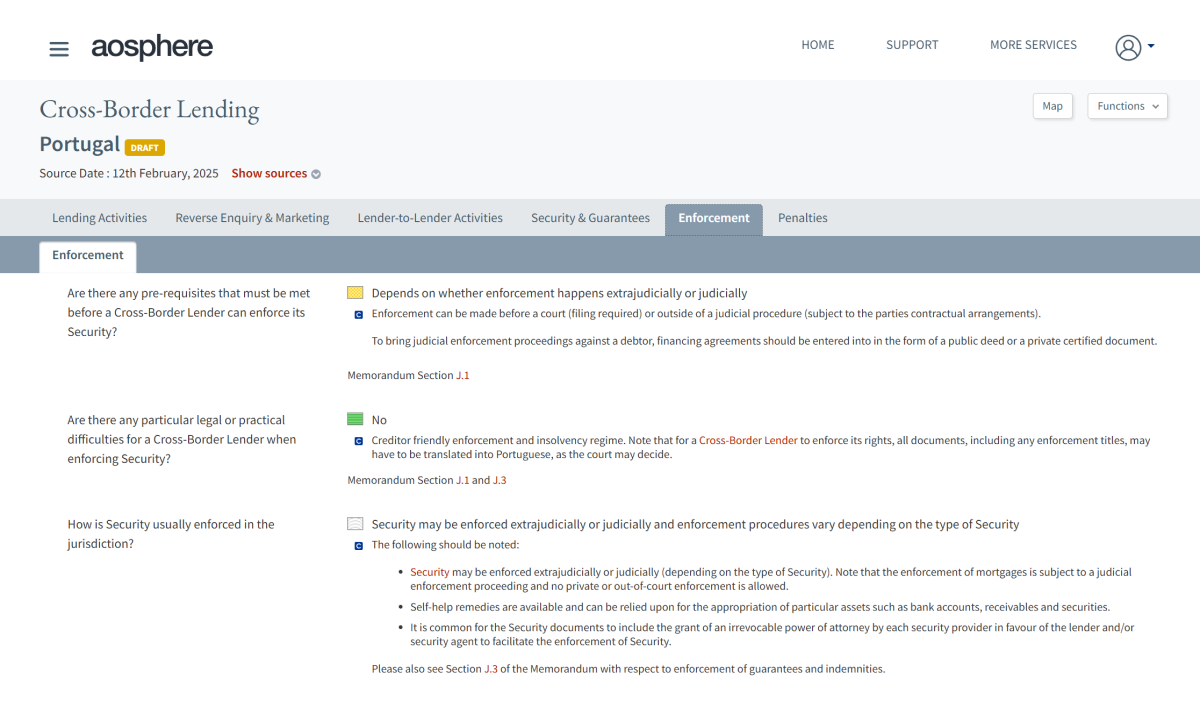

Key issues relating to enforcement

- triggers for being able to enforce and particular red flags to be aware of

- availability of “self-help” remedies

- practical commentary on experiences of creditors enforcing rights in the jurisdiction

- analysis regarding choice of law/submission to jurisdiction clauses and enforceability of foreign judgements

- availability of a restructuring regime/toolkit within the jurisdiction

Restrictions/limitations on obtaining benefit of a guarantee/indemnity in relation to the loan

- analysis of impact of upstream, cross-stream or downstream guarantee

BRP Tax consider how lending activities are viewed from a tax perspective in the jurisdiction of the borrower with a particular focus on withholding tax and stamp duty.