A bird's eye view from aosphere

If you hold shares in a company which becomes subject to a takeover, this may prompt additional disclosure requirements under the takeover rules of a country – quite separate to the substantial shareholding rules. There are around 20 takeover disclosure regimes that are covered by Rulefinder Shareholding Disclosure. To give some perspective on just how nuanced these rules can be, we’ve taken a few recurring points of divergence from across the world.

1. Share for share rules

A share for share offer, or securities exchange offer, means an offer in which the consideration includes securities of a bid party. Some countries require disclosure of transactions in the company whose securities are used as consideration in the public takeover bid as well as the target – an example of where this is the case is Hong Kong. Always check whose securities you need to disclose transactions in. By contrast to Hong Kong, in Cyprus bidder disclosures are required regardless of a securities exchange.

2. Unlisted issuers

In some cases the rules might also cover unlisted target issuers. An example of this is Singapore, where the Singapore Takeover Code also considers certain unlisted public companies and unlisted registered business trusts. Changes to the UK Takeover Code recently removed a private company residency test (which applies to certain Code companies that are not UK quoted). This is subject to a transition period.

3. Lower thresholds than major shareholding regimes

Takeover rules may require disclosures relating to holdings much lower than the market disclosure rules for substantial shareholdings. The UK Takeover Code requires that persons interested in 1% or more of any class of relevant securities of the offeree or a securities exchange offeror must make disclosures.

4. Data/lists

Some regulators produce lists of companies subject to takeover actions, for example Austria, which facilitates tracking takeover disclosures. However, others do not produce publicly available takeover lists, for example Australia and market participants may have to check alternative sources such as company announcements.

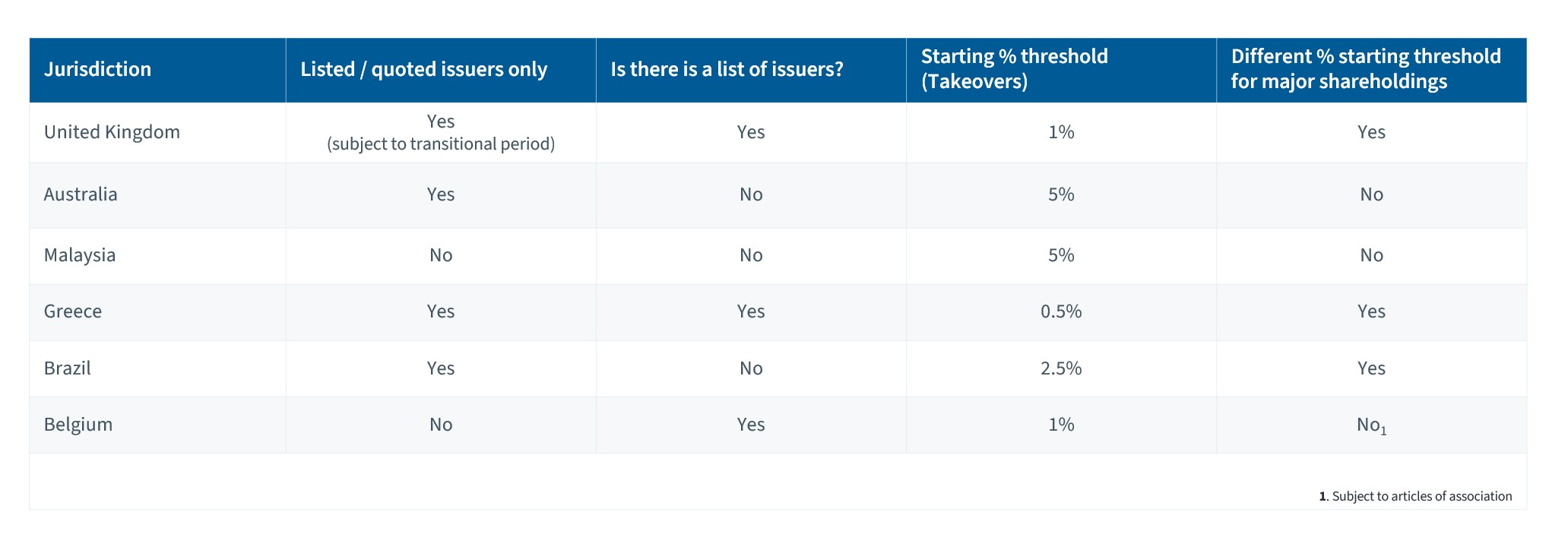

Summary table

When we compare some of these nuances, including listing scope (who the rules apply to) and starting thresholds (at what % holding you may need to make a disclosure), you can see one rule does not fit all. Here is an extraction table that pulls some of these differences together for illustrative purposes.

Final remarks

You must always check the jurisdiction rules for each country, because these rules are not uniform in their approach. It is also worth being aware of extraterritoriality. For example, when considering whether you are a relevant person for the UK rules, that relevant person isn’t determined or excluded by virtue of their location and neither is the securities exchange offeror. So, for example, where a UK offeree is involved, a US investor in a US securities exchange offeror would need to consider their UK takeover disclosure requirements – and as we have mentioned above, the threshold for a relevant interest is low. With starting disclosure thresholds even lower than major holdings disclosures and sensitivities regarding in-scope securities and disclosable bid parties, the devil remains in the detail for compliance professionals.

How aosphere can help

Rulefinder Shareholding Disclosure provides comprehensive analysis of shareholding disclosure rules in 100+ jurisdictions, covering substantial shareholdings, short selling, sensitive industries, takeovers, and issuer requests.

The detail is there for those who need it, but we also provide summaries and threshold apps for those who don’t.