In this article, we discuss the complexity of short position reporting in jurisdictions with low threshold-based regulatory regimes, and the practical issues to consider for firms fulfilling their reporting compliance obligations.

Rulefinder has updated its Short Positions Global View infographic to include at-a-glance details on gross position reporting in Canada and the new USA rules effective January 2025.

The infographic also gives an overview of key characteristics of the net short position reporting regimes in the EU, UK, Australia, Hong Kong, Japan, Singapore and South Korea. Through the in-depth analysis of short selling covered in Rulefinder Shareholding Disclosure, we know that there are low threshold-based net short position reporting regimes in the EU and the UK and in several APAC countries (Hong Kong, Singapore, Japan, South Korea and Australia).

The rules can appear similar, for example:

- most rules prohibit the naked short selling of shares and will only allow short sales where the sales is covered (e.g. by securities lending arrangements)

- rules may allow certain exemptions based on capacity exemptions (e.g. market maker) or settlement certainty (e.g. rights to recall lent securities)

However, there are many differences between the regimes even where these similar principles are engaged (e.g. for market maker exemptions different conditions for use will apply in different countries). For disclosure purposes, the regimes are often quite different to begin with. There is no common threshold. The calculation may be required daily or weekly.

Here are some key questions for firms to consider when analysing their disclosure obligations, along with some illustrative, non-exhaustive, examples sourced from Rulefinder:

1) Is there a restriction on naked short sales, and if there is, is covered short selling permitted? What does cover mean?

As an example, Singapore does not apply a naked short selling restriction.

2) Are there any exemptions that apply to naked short selling, or any exclusions from the definition of short selling that apply?

As an example, Japan has many exchange traded exemptions for share sales e.g. shares of sales allocated by share split.

3) What is the nature of short selling exemptions?

As an example, a market maker on The Stock Exchange of Hong Kong Limited (SEHK) may sell short securities (regardless of whether they are ‘designated securities’) in its capacity but has an extra day for covering the short position.

4) What types of interest contribute to long or short interests in shares, for share disclosure?

As an example, the EU and UK Short Selling Regulation both set out very detailed calculation rules for share position disclosure. This is not typical for other rules sets.

5) What is the disclosure threshold based on? Is it a percentage of share capital? It is a per share class test? Is market value relevant?

As an example, South Korea has a two tier disclosure test and which test applies depends on the Korean Won (KRW) value of the position.

6) At what point do you calculate your net short position? Is it daily? Or weekly on a set day?

As an example, in Australia, as long as the seller holds a short position in that section 1020B product above the reporting threshold, the seller is obliged to provide daily reports to the Australian regulator (ASIC) on the size of this short position.

7) How do you make disclosure? Will you need to be registered for a portal or is it by other means?

As an example, in the EU, each Member State is responsible for establishing its own procedure for notifications and public disclosures, including standard forms.

8) How long do you have to make disclosure?

As an example, in the EU, net short positions must be calculated at midnight at the end of the trading day on which the person holds the position and notified not later than 15.30 on the following trading day. Times are calculated according to the time in the Member State of the competent authority to whom notification is made.

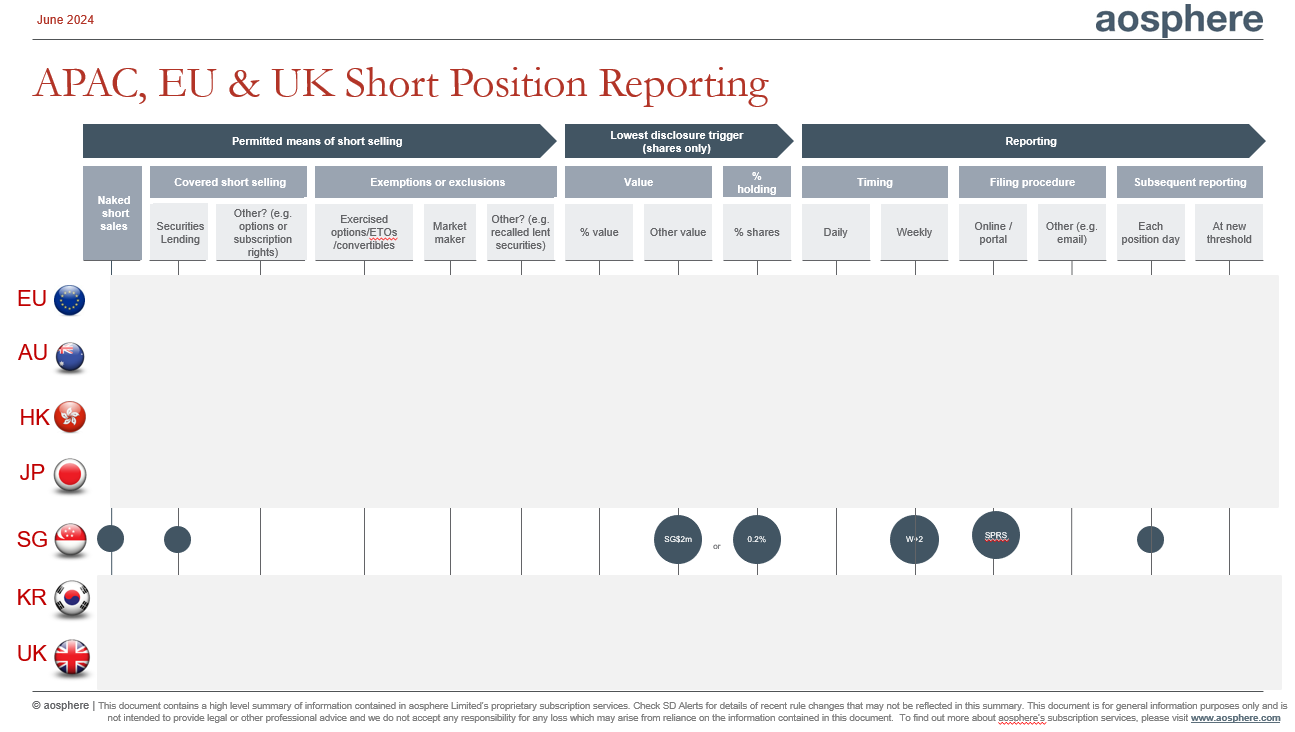

The Short Position Reporting Global View

Rulefinder Shareholding Disclosure analyses these net short position-reporting regimes in-depth, along with major shareholding disclosure requirements, industry acquisition limits, enhanced disclosure during takeovers and issuer initiated disclosure requests.

To aid cross-jurisdictional analysis, subscribers can compare treatment of the rules across regions in a consistent format using the in-built Compare feature available within Rulefinder. In addition, we have made it easier for in-house legal and compliance users to understand cross-border comparisons of net short position reporting with the introduction of a visual representation of the global view of net short positions.

Sample from the Short Position Reporting Global View:

What am I looking at?

Our Global View (Singapore only in this sample) first flags to users how they can conduct short selling (can you make naked short sales?; do you cover your sales and how?; are there any exemptions?). It then goes on to discuss disclosure obligations (what is the trigger(s) for disclosure?; what is the timing for disclosure?; how often should positions be assessed?; how do you make a submission?). Our full Subscriber infographic gives this detail, for all 7 net short position jurisdictions as well as for the gross short position rules in Canada and the USA, and also includes detailed points to note and a user guide for aosphere’s in-report tools.

How aosphere can help

Launched in 2008, Rulefinder Shareholding Disclosure provides comprehensive analysis in over 100 jurisdictions, and is used by over 450 financial institutions as an alternative to bespoke legal surveys.