What happens if we miss a reporting obligation, file too late, or get the filing wrong? What actions can regulators take, and what actions do regulators take? The question of enforcement actions is one clients frequently ask us about in the field of shareholding disclosure.

In this Q&A aosphere senior lawyer, Kirsty Simon explains why it is so important for firms to be aware of the risks of non-compliance. Kirsty has worked exclusively on the Rulefinder Shareholding Disclosure product for the last thirteen years. Our interviewer for this article is Charlotte Hayward, Head of BD (Americas) at aosphere.

Kirsty, what powers do regulators currently have to impose enforcement actions for non-compliance with major positions reporting rules and short selling rules?

There is a lot for clients to think about when complying with shareholding disclosure rules globally. From thresholds, timing, aggregation and instruments in scope, all the way through to how you actually disclose a position. An overarching question from clients managing their risk is… what happens if we breach the rules?

Regulators have different powers available to them, e.g. across much of Europe the enforcement actions include fines of up to €10 million or 5% of the annual turnover of the discloser and a suspension of voting rights for both the legal and beneficial owners.

In Brazil as well as warnings and fines, the regulator can impose disqualification from positions of seniority in public issuers in Brazil, and temporary prohibition (up to ten years) from engaging in transactions involving the listed shares. This is against a backdrop of a short reporting deadline for disclosures and fines for repeat offenders being trebled.

In South Korea enforcement actions for illegal/naked short selling include criminal penalties, (imprisonment for at least one year). Also maximum criminal fines for illegal short selling equal to at least three times but not exceeding five times the amount of profits earned from such violation and/or losses avoided by such violation, not exceeding KRW 500 million. In September 2024, short sale reforms were passed by the National Assembly which are due to come into effect at the end of March 2025. The revised laws include strengthened criminal penalties for illegal short selling activities, including an increase in fines to four to six times the amount of unfair profit and diversification of enforcement actions which will include restrictions on financial investment product transactions and restrictions on the appointment and tenure of directors of listed companies for up to 5 years).

It is important to note that it is not just heavy financial fines and imprisonment that investors need to worry about; reputational risk relating to a public sanction can be more severe and of the highest priority to many of our subscribers. Although not all enforcement actions are published, it is advisable that clients act as if they are as the risk of reputational damage is so great.

Great. And globally we already ask local counsel for this info on the enforcement powers available to regulators as part of Rulefinder SD. Do you see any trends with regards to regions/jurisdictions – what’s the norm, and what are the exceptions in terms of types of censure?

Yes this is the benefit of the Rulefinder product as it allows you to compare enforcement actions across over 100 jurisdictions in the areas of Substantial Shareholdings, Sensitive Industries, Takeovers, Issuer Requests and Short Selling.

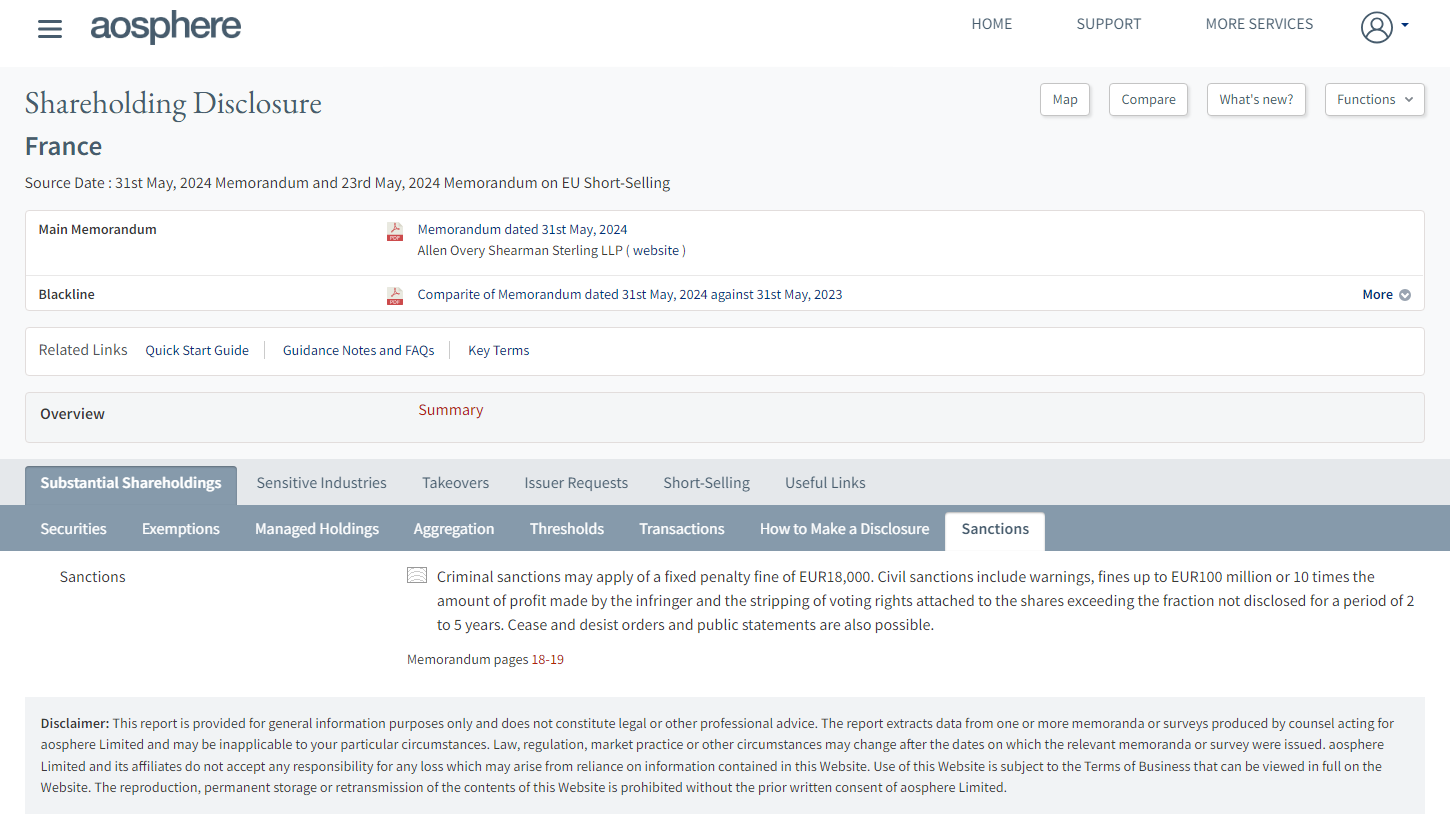

Sample summary of on-screen analysis from Rulefinder Shareholding Disclosure France (published May 2024)

And how can firms get a feel for when enforcement actions are actually imposed?

Great question. We have a useful resource which goes beyond what enforcement actions a regulator can impose, and tracks public sources for examples of recent regulatory enforcement. The Shareholding Disclosure Enforcement Actions tracker is very useful in allowing subscribers to identify trends and note any regulators who are particularly active. We also notice certain trends in regulators who apply the rules very stringently for example imposing enforcement actions if a name is misspelt on a form or those who are more lenient. The subscriber feedback we have received is that the tracker allows investors to build a picture of how a particular regulator approaches fines and any jurisdictions where they need to be extra careful.

For example Germany’s regulator BaFin is well known for being strict on even small mistakes made on disclosure forms. The Danish FSA has previously highlighted that major shareholders make a number of significant mistakes when using updated versions of standard forms for reporting major shareholder announcements. The study also identified that there were errors in the completion of the standard form in 65 per cent of the reports made by major shareholders when a new version of the standard form was issued. This shows just how easy it is to get things wrong and that regulators are taking note.

And how do we monitor for this type of content?

Some jurisdictions do not publish enforcement actions and not all regulators have dedicated web pages for enforcement actions so one of the key challenges in tracing enforcement actions is sourcing reliable data in these jurisdictions. We have a monitoring system in place as part of our daily horizon scanning so have been able to pick up enforcement examples through our existing channels. We focus on tracking major position, takeover and short selling reporting sanctions. The tracker is a way of us providing subscribers with a snapshot of examples of real life enforcement actions being imposed by regulators.

What kind of information can firms access through the Enforcement Actions Tracker?

We really wanted to present the information we had in a user-friendly way, so we have recently upgraded the tracker to a grid format. This allows subscribers to manipulate the data themselves to sort and compare by sector, jurisdiction or enforcement action amount. We also decided that in addition to showing the original currency of the fine, we would include the equivalent GBP value as at the date of each fine so that subscribers can filter amounts from largest to smallest and see which jurisdictions have the largest fines and whether some jurisdictions impose generally higher fines for equivalent breaches.

We have added an ‘Additional Information’ pop up comment to the spreadsheet, which we use to add any interesting commentary points for example; was it the first time the regulator had imposed a sanction of this type, or what was the compliance mistake, which led to the fine being imposed? Has the regulator told us why it was imposed?

We have seen some interesting examples, which brings home the variety of sanctioning powers regulators have at their disposal and the sort of mitigating factors they will take into account in lessening a fine.

Cases where regulators explain how they reached their decision help bring the rules to life and can give an insight into regulators’ expectations of position holders.

For example in June 2024 the Norwegian FI issued a fine for a violation of the notification requirement under section 3-5 of the Norwegian Securities Trading Act and article 5 cf. article 9 of Regulation (EU) No 236/2012 by not notifying the FI in accordance with the SSR of the relevant net short positions. In deciding the penalty the FI considered the length of the unclosed net short position, (the position remained unchanged/unclosed for more than three years), and the size of the net short positions which were unreported/unclosed (over the 0,5% threshold). The fact that the FI’s inquiries revealed two other unreported positions was considered as an aggravating circumstance. In its assessment, the FI also considered the implications the unclosed net short position had towards the information available to the marked participants.

Sample content from the Enforcement Actions Tracker, November 2025

What conclusions can organisations take from seeing the range of sanctions being taken?

With increasing legal changes coming into force in recent years, it is easy for mistakes to happen. Monetary fines can be painful but the reputational risk related to the public sanction of the firm should be considered more severe. Your business’s reputation is your most valuable asset, especially if you are a bank or financial institution.

How aosphere can help

Launched in 2008 and used by over 450 financial institutions as an alternative to bespoke legal surveys, Rulefinder Shareholding Disclosure provides comprehensive analysis in over 100 jurisdictions and can help you understand the rules themselves and the implications of non-compliance at a global level.