Overview

Shareholding disclosure rules can be complicated, and this is particularly true for investment mangers making disclosures in respect of their managed holdings. Before considering the thresholds and any applicable exemptions, an investment manager needs to know whether its discretionary mandate triggers the disclosure rules in the relevant jurisdiction.

Where the investment manager has to make a disclosure, there are further questions to think about and, unfortunately, no universal answers. In this article, we highlight the key questions that investment managers can ask, to cut through the tangle of rules and understand their shareholding disclosure obligations.

How does an investment manager determine whether it has a disclosable interest?

The first consideration is the type of mandate the investment manager has. The terms of a mandate may give the investment manager both investment and voting discretion or it may split these discretionary elements with another entity, such as a sub-manager. The question of whether an entity has voting and/or investment discretion in a given scenario will of course depend on the facts of the particular managed holdings arrangement, but the same mandate can produce different disclosure outcomes depending on the jurisdiction.

In the EU, the Transparency Directive (TD) stipulates that voting discretion is a disclosable interest. Therefore, in a typical discretionary investment management scenario including voting discretion, the investment manager will have a disclosable interest. This is straightforward enough, but be aware that other complexities arise in the EU – see the separate questions on the following page.

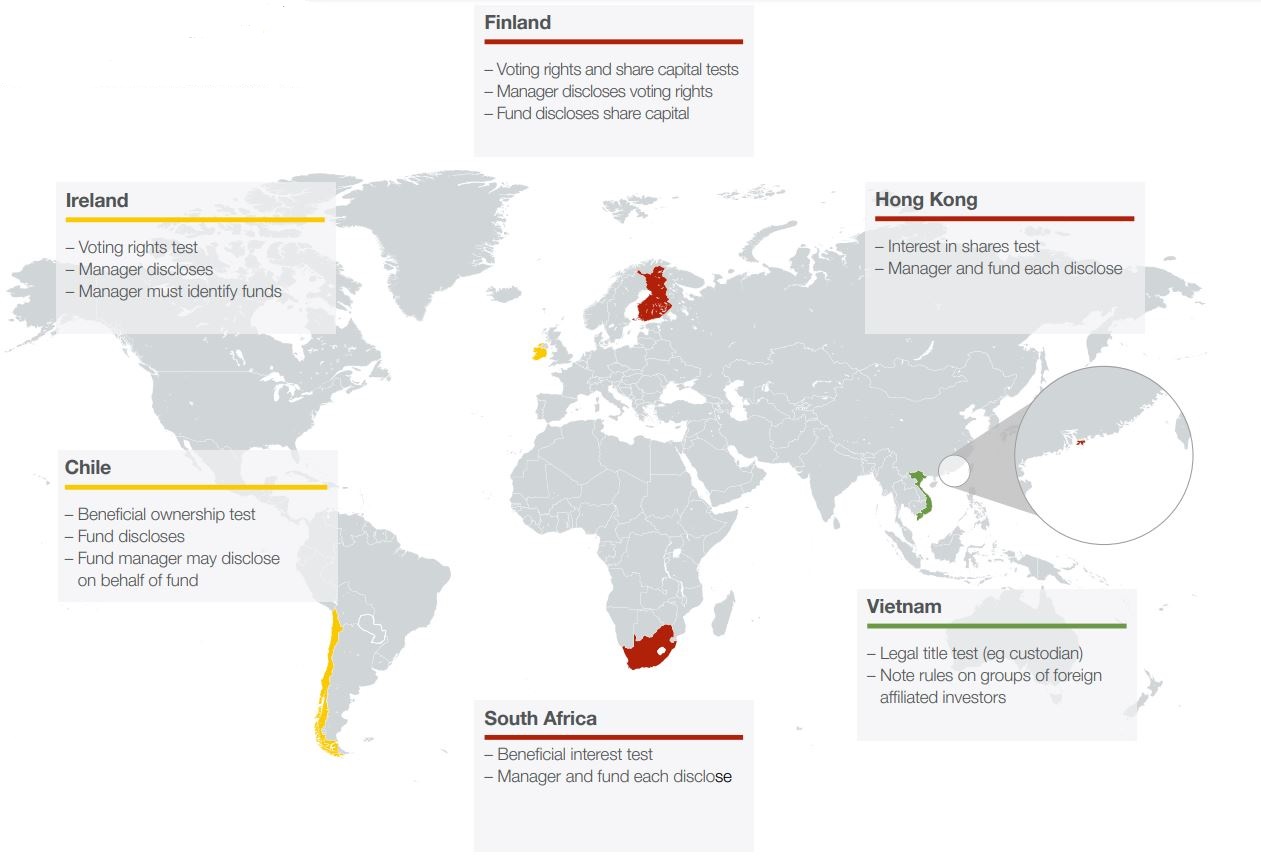

Outside the EU, the disclosure triggers are more varied and, therefore, the position becomes considerably more complex for the investment manager. As well as voting control, a disclosable interest may arise, for example, on the basis of legal title (eg Vietnam), a beneficial interest (eg South Africa), or some broader interest in shares (eg Hong Kong). Some of these regimes will capture investment managers with voting and/or investment discretion over their managed holdings. However, terms such as “beneficial interest” or “interest in shares” have specific local meanings, producing different disclosure outcomes for investment managers.

If a manager doesn't have voting discretion for its mandates, do the major shareholding rules still apply?

It is a common misconception that if an investment manager does not have voting control then shareholding disclosure rules do not apply to its holding of managed securities. This likely stems from the fact that in the EU the TD regime is based on voting control, so an investment (buy/sell) only mandate will not give rise to a notification for the investment manager. But as mentioned in the first question, outside the EU each jurisdiction will have its own disclosure rulebook. Investment discretion may amount to a disclosable interest in shares and therefore mandates that give investment discretion only can trigger a shareholder notification.

The map shows how the same investment management scenario can result in different disclosure outcomes depending on the jurisdiction

In this scenario the manager has voting and investment discretion. A custodian holds the shares on behalf of the fund. More detail in Rulefinder Shareholding Disclosure, including additional scenarios, eg managed accounts, use of a sub-manager. Rules on corporate aggregation also have to be taken into account as they may affect the disclosure position in practice.

Does the investment manager need to provide any fund information in the disclosure form?

If an investment manager has a notifiable interest, it needs to know what fund-related information it should include in its notification. Should it identify the funds and, if yes, is it all funds or only those which have reached the lowest disclosure threshold?

In the EU, ESMA’s standard notification form provides helpful clarification on this point: the general picture is that the investment manager is required to list any funds which have reached the lowest disclosure threshold.

Outside the EU, again the position is more diverse, and even if the notification forms do not expressly ask for this information, the wording of the relevant legislation might point to the investment manager needing to identify all funds.

Be aware of jurisdiction-specific nuances. In some jurisdictions changes to the list of funds, without any change to the investment manager’s aggregated holding, can prompt the need for a fresh disclosure.

What about the fund and any sub-manager? Do they have to disclose?

If the investment manager is required to make a disclosure, don’t assume that the fund and sub-manager are off the hook – multiple disclosures may be required in respect of the same managed holdings. For example, in jurisdictions where disclosure is triggered by a wide range of interests in shares, such as Hong Kong, the investment manager, fund, custodian and sub-manager may each have a separate disclosure obligation.

In the EU this is where national discrepancies arise. In some jurisdictions, a fund has a separate disclosure obligation in addition to the investment manager, either under a share capital test or as the direct shareholder.

What happens if an investment manager gets it wrong?

A variety of sanctions can apply to breaches of shareholding disclosure rules. In the EU, sanctions include fines, suspension of voting rights and public statements by the regulator. In the rest of the world, sanctions may be more severe and can include criminal penalties and potential personal liability.

With tough sanction powers available to national regulators, it is essential for investment managers to be on top of these rules.

Key takeaways for investment managers

-

It is important to understand the different disclosure triggers in the relevant jurisdictions.

-

Outside the EU, local rules may require disclosure even if the investment manager has no voting discretion.

-

The investment manager’s notification form may need to include information on holdings at the individual fund level.

-

Remember that the fund and any sub-manager may also have a disclosure obligation in respect of the managed holdings.

How aosphere can help

Launched in 2008, Rulefinder Shareholding Disclosure provides comprehensive analysis in over 100 jurisdictions, and is used by over 450 financial institutions as an alternative to bespoke legal surveys.